Understanding Tax on ₹12 Lakh Income in India (Tax Year 2025-26)

CA Meet Dhrangadhariya

CA Meet Dhrangadhariya  December 17, 2025

December 17, 2025

CA Meet Dhrangadhariya

CA Meet Dhrangadhariya

Table of Contents

Table of Contents

Income tax can be confusing, especially when new rules come into play. Budget 2025 brought one of the biggest changes in personal income tax in recent years. If you earn ₹12 lakh a year, here’s what you need to know about your tax liability under the Income Tax Act 2025.

The government revised the income tax structure effective for financial year 2025-26 (assessment year 2026-27). A key feature is the higher rebate and adjusted slab rates to boost disposable income for individuals.

Under the new tax regime:

Income upto ₹12 lakh is eligible for a full tax rebate under Section 87A, which essentially reduces your tax liability to zero.

This means a person earning ₹12 lakh in a year does not pay any income tax if they choose the new tax regime.

Here’s the idea:

The slabs start at zero tax for the first part of income.

Even though regular slabs would tax portions of income above ₹4 lakh, the rebate cancels the tax completely up to ₹12 lakh.

This change is a major relief for middle-income earners and increases take-home salary.

If you’re a salaried employee:

You receive a standard deduction (around ₹75,000) before calculating taxable income.

After standard deduction, your taxable income might effectively fall below ₹12 lakh even if your gross salary is slightly above that.

In practice, many salaried individuals earning up to ~₹12.75 lakh also pay zero tax because of this deduction plus the rebate.

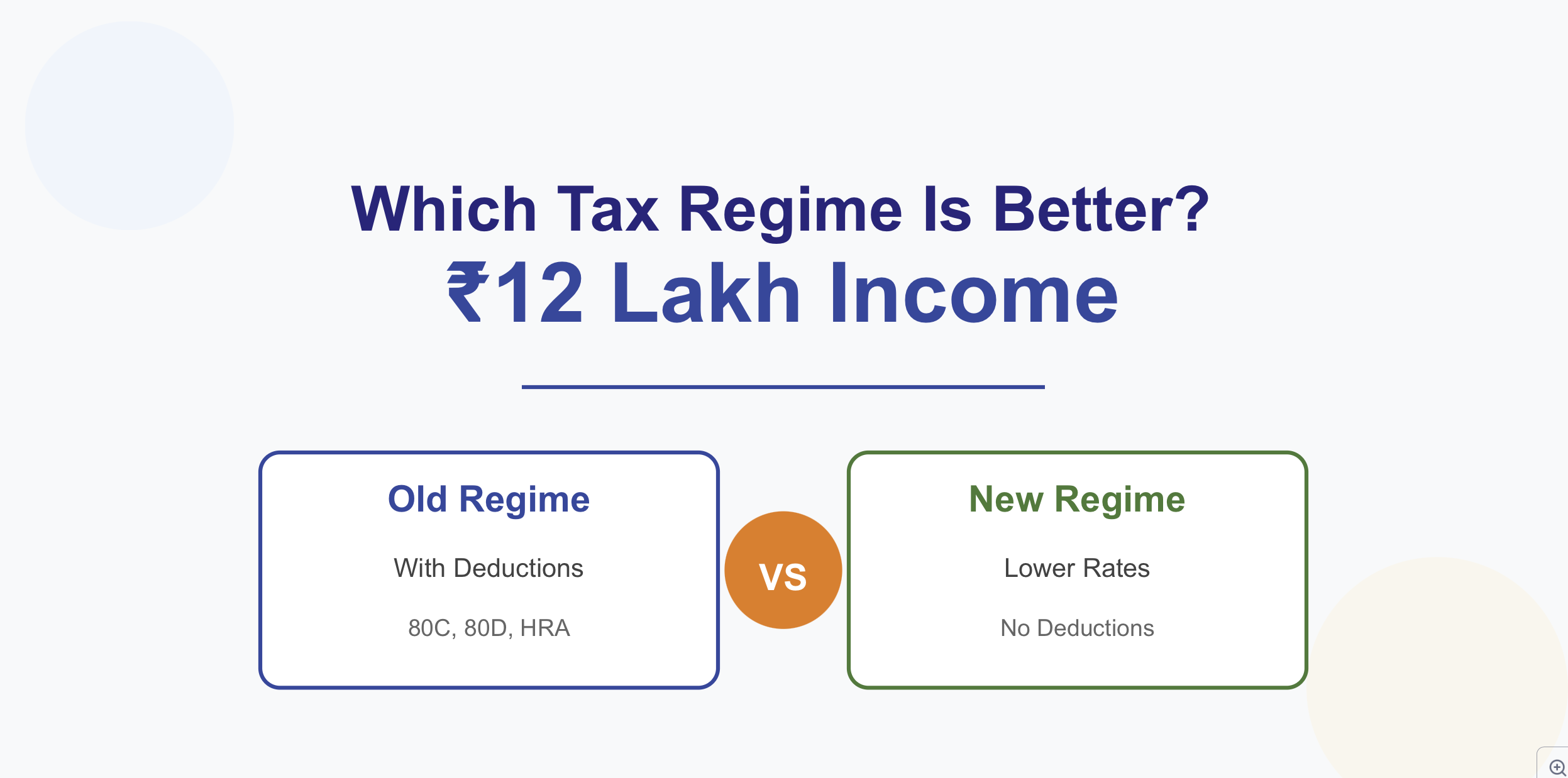

You can choose between the old tax regime (with exemptions and deductions like 80C, HRA, 80D) and the new simplified regime. For someone at ₹12 lakh:

Under the old regime, you will have tax liability after standard slabs and only enjoy exemptions you claim.

Under the new regime, the tax rebate wipes out tax up to ₹12 lakh, making it generally more beneficial for many people without heavy deductions.

Imagine your gross salary is ₹12 lakh:

You get standard deduction (₹75,000 for a salaried person).

Your taxable income becomes ₹11,25,000.

Section 87A rebate cancels your tax liability on that amount under the new regime.

Final tax payable is zero.

This drastically increases your monthly take-home pay compared to previous years.

|

Particulars |

Old Tax Regime |

New Tax Regime (2025) |

|---|---|---|

|

Gross Annual Income |

₹12,00,000 |

₹12,00,000 |

|

Standard Deduction |

₹50,000 |

₹75,000 |

|

Income After Standard Deduction |

₹11,50,000 |

₹11,25,000 |

|

Other Deductions (80C, 80D, HRA etc.) |

Assumed ₹1,50,000 |

Not Applicable |

|

Taxable Income |

₹10,00,000 |

₹11,25,000 |

|

Tax Before Rebate |

₹1,12,500 approx |

₹56,250 approx |

|

Section 87A Rebate |

Not Available |

Available up to ₹12 lakh |

|

Final Tax Payable |

₹1,12,500 + cess |

₹0 |

|

Best Suited For |

People with high deductions |

Most salaried individuals |

Step 1: Gross Income

₹12,00,000

Step 2: Standard Deduction (Salaried)

₹75,000

Step 3: Taxable Income

₹12,00,000 − ₹75,000 = ₹11,25,000

Step 4: Tax as per slabs

Tax calculated as per new slab rates

Step 5: Section 87A Rebate

Since taxable income is below ₹12,00,000, entire tax is rebated

Final Tax Payable

₹0

Assumptions

Standard deduction: ₹50,000

80C deduction: ₹1,50,000

Taxable Income

₹12,00,000 − ₹50,000 − ₹1,50,000 = ₹10,00,000

Tax Calculation

Up to ₹2.5 lakh: Nil

₹2.5 lakh to ₹5 lakh: 5% = ₹12,500

₹5 lakh to ₹10 lakh: 20% = ₹1,00,000

Total Tax

₹1,12,500

Plus 4% cess = ₹4,500

Final Tax Payable

₹1,17,000 approx

Under the new tax regime, income up to ₹12 lakh is completely tax free due to Section 87A rebate.

Salaried employees can effectively earn up to ₹12.75 lakh with zero tax because of the higher standard deduction.

The old regime only benefits those with large deductions like home loan interest or major investments.

For most individuals earning ₹12 lakh, the new tax regime is clearly more beneficial.

The 2025 tax changes are designed to benefit middle-class taxpayers by reducing or eliminating tax on incomes up to ₹12 lakh. For many people with this income level, the best option is the new tax regime with the rebate, especially if you don’t have large deductions to claim.

Always consider using a tax calculator or consulting a tax professional to determine what’s best for your individual financial situation.

CA Meet Dhrangadhariya

CA Meet Dhrangadhariya

Hatim Bharmal

Hatim Bharmal

Sohil Panwala

Sohil Panwala  CA Meet Dhrangadhariya

CA Meet Dhrangadhariya